When we look at financial statements, it’s tempting to treat them as the objective truth. After all, the numbers are audited, standardized, and presented with an air of authority. But what if those numbers aren’t the full picture? What if they’re not lies, exactly, but not the truth either?

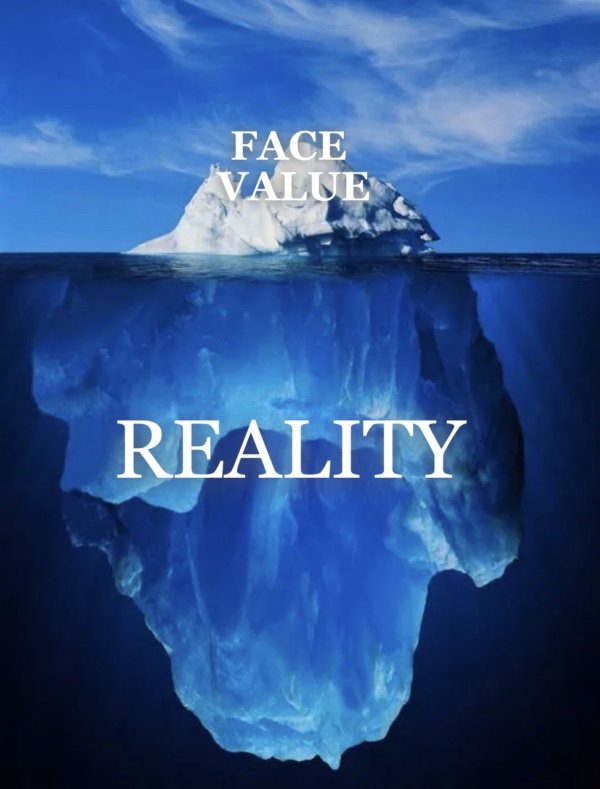

Icebergs, as many of us know, are more than 90% submerged in water, whereas the other 10% is visible at sea level. Why do I mention this?

Financial statements are best understood as interpretations of reality, essentially shaped by accounting rules, assumptions, and human judgment. They aim to describe what’s happening inside a business, but they don’t, and are unable to capture everything perfectly. This is why misleading, or should I say, deceptive, financials don’t all come from the same place. In practice, they usually fall into three broad categories: outright fraud, legal but aggressive manipulation, and honest or unintentional misrepresentation.

The goal of financial intelligence is not to predict the future perfectly or to catch every bad actor. Instead, it’s about learning to ask better questions. Why do the numbers look the way they do? What assumptions are being made? And what might be missing from the story being told?

Total Fraud — When the Numbers Are Fiction

At its most extreme, financial misrepresentation occurs when numbers stop reflecting business reality altogether and become deliberate fabrications. In cases of total fraud, management knowingly falsifies financial data, hides losses, or invents performance to mislead investors and stakeholders. This is not a gray area of judgment or interpretation—it is a clear violation of accounting rules and the law.

These companies often appear unusually successful on paper. Earnings seem smooth and consistent, even in volatile industries. Profits rise steadily, yet cash flow fails to keep pace. Sometimes, it isn’t until years later — after a sudden restatement or collapse — that the truth becomes visible. By then, investors who trusted the surface-level numbers have already paid the price.

Case Study: WorldCom

WorldCom’s collapse is one of the clearest examples of how fabricated financial statements can disguise a failing business. During the late 1990s and early 2000s, WorldCom reported steady earnings growth despite increasing competition and weakening fundamentals in the telecommunications industry. On paper, the company looked stable and profitable.

Behind the scenes, however, WorldCom was capitalizing ordinary operating expenses, such as line costs1 paid to other telecom providers. These costs should have been recorded as expenses on the income statement, reducing profits. Instead, they were moved onto the balance sheet as assets, artificially inflating earnings and EBITDA.2 Cash flow, meanwhile, quietly deteriorated.

Investors and analysts focused heavily on reported earnings and adjusted metrics, trusting that the accounting treatments were legitimate. Few questioned why a capital-intensive telecom company could report growing profits without generating the cash to match them. When the fraud was eventually uncovered, more than $11 billion in expenses had been improperly classified, revealing that WorldCom had been unprofitable for years.

The lesson from WorldCom isn’t just that fraud exists. It’s that even blatant warning signs can be and are often ignored when financial statements look consistently “strong,” and no one challenges how those numbers were created, especially when those numbers may seem to be in favor of investors.

Red flags to watch for:

- Earnings growth without corresponding cash flow growth

- Unnaturally smooth earnings over long periods

- Management that discourages transparency or explains complexity vaguely

Legal Manipulation — When the Numbers Are Technically Right but Misleading

Not all misleading financial statements are illegal. In fact, some of the most dangerous cases involve companies that follow accounting rules — but push them to their limits. This form of manipulation relies on judgment calls, timing differences, and optimistic assumptions, often justified as “aggressive accounting.”

The problem isn’t that the numbers are wrong. It’s that they create a distorted impression of economic reality. Revenue may be recognized earlier than it should be. Expenses may be delayed. Adjusted or non-GAAP3 metrics may be emphasized to tell a more favourable story. Over time, the financial statements drift further away from what the business is actually earning.

Case Study: Xerox

Xerox provides a classic example of legal but misleading accounting practices. In the late 1990s, the company accelerated revenue recognition from long-term equipment leases. By recognizing future revenue earlier, Xerox was able to boost short-term earnings and meet market expectations.

The financials looked healthy, but the underlying business was weakening. Growth was being pulled forward from the future rather than generated organically. Eventually, the gap between reported performance and economic reality became too large to ignore, leading to regulatory action and restatements.

What makes cases like Xerox especially instructive is that nothing initially appeared “wrong” in a technical sense. The accounting complied with existing rules. But the story told by the numbers was misleading.

Red flags to watch for:

- Frequent changes in accounting policies or assumptions

- Large gaps between GAAP and non-GAAP earnings

- Management explanations that rely on “one-time” adjustments every year

Unintentional Misrepresentation — When the Numbers Mislead Without Bad Intent

Sometimes, financial statements mislead not because of fraud or manipulation, but because accounting rules fail to capture economic reality, especially in fast-changing industries. In these cases, the numbers may be accurate, yet still incomplete or misunderstood. As investors, we must understand that all, or at least a large portion, of financial statements contain assumptions, estimates, and blind judgment calls due to various reasons. When operating at a large scale, keeping track of precise details becomes nearly impossible: human resources, operating costs, payments, asset usage, and, in the case of Nvidia, depreciation.

Accounting frameworks were largely designed for industrial-era businesses, where assets depreciated slowly, and growth was incremental, slow, and unsteady.

Applying the same rules to modern, innovation-driven companies can create distortions. Think of it as comparing computers back when they were still in development, versus Nvidia’s graphics cards nowadays. Investors may draw incorrect conclusions by relying too heavily on traditional metrics like earnings per share or price-to-earnings ratios.

Example Discussion: Depreciation, Nvidia, and Model Mismatch

Michael Burry, a well-known American investor, highlighted how depreciation and capital intensity can distort reported earnings. Depreciation schedules, for instance, are accounting estimates — not economic truths. If assets lose value faster than accounting assumes, profits may be overstated.

Take Nvidia, for example. In Nvidia’s case, rapid innovation cycles and high upfront investment complicate traditional financial analysis. NVIDIA recently extended the depreciation life of certain assets from approximately three years to six years. While legally permitted under accounting standards, such a move lies within the “gray area.” This change reduces annual depreciation expense and increases reported profits without actually altering the company’s actual cash flow.

The issue here isn’t fraud. It is, in reality, a model mismatch within somewhat reasonable boundaries. Nowadays, accounting rules struggle to keep up with businesses where technology evolves faster than one can get used to.

Red flags to watch for:

- Accounting rules that feel outdated for the business model

- High-growth companies whose earnings don’t reflect competitive strength

- Overreliance on single metrics without broader context

How to Read Financial Statements More Intelligently

Not all misleading financial statements are criminal, and not all accurate financial statements are informative. Financial intelligence begins with understanding that numbers tell a story — but not the whole story.

Instead of asking whether the numbers are “right,” a better question is why they look the way they do. What assumptions are being made? What incentives are driving management behavior? And how well do the accounting rules fit the business model?

Reading financial statements intelligently means combining:

- The financial statements by face value

- An understanding of the business model

- Awareness of incentives and management behavior

The goal isn’t cynicism. It’s skepticism. Question yourself.

(THE END)

Footnote 註釋:

- Expenses a business incurs to generate revenue and appear above operating income or gross profit on financial statements.[↩]

- EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization.[↩]

- Generally Accepted Accounting Principles[↩]